As we approach financial independence and taking flight ... a common question is ... Why Spain? Why Granada?

Well ...let’s back up a few years ... when we initially started talking about financial independence we decided we would like to move to a better climate / place with seasons (versus our very hot home of Houston) eventually, and we had our eyes set on Colorado as a possibility (and considered Oregon). We were also hoping for a place we could enjoy the outdoors more. These still may be on the table ... eventually.

Fast forward some time ... the kids ended up at my school and in the Dual Language program (Spanish / English). This was never in the plans, but it has been the best thing for us (having them at school with me!) and them (learning a second language!). Their teachers and classmates have been fantastic, and we couldn’t have asked for a better experience. I don’t know the timing of it, but eventually Erik said ... well, why not Spain? Full immersion in the language and culture for them and all of us!

So why Spain versus another country that is closer (hello, Mexico!) ... Maybe we will further explore some countries closer to the US, but as far as why Spain ...

-Climate

-Easy access to explore Europe (also beyond Europe ... I am looking at you, Morocco!).

-Culture Shock ... go to a place different than what we currently know / different area of the world.

-Cost of living.

(Also something else to throw in the mix ... why abroad? To be honest, I am not sure the US public education system is the best place for my kids right now ... safety and the testing culture are two reasons so that has definitely played into this decision. But that is probably for a future post, but you can see our post on World Schooling here.).

Why Granada?

-Climate (Yes, the winters get colder than we are use to in Houston, but we are looking forward to that change!). And anything is cooler than Houston (surface of the sun).

-An hour give or take from the Sierra Nevada mountains (snow / skiing / etc.)! This is a link to their ski resort in the Sierra Nevada mountains (things to do for families).

-An hour give or take to the beach (or really I should say beaches!). (Granada is located in Spain’s Andalucia region along Costa Tropical with quick access to many beautiful beaches. Being located that close to snow and the beach is a top selling point for all four of us - that is for sure!).

-Access to the great outdoors / hiking, etc.

-Walking City / Public Transportation

-I’m sure we might find some similarities to what we are use to in Houston, but overall we like that it is so different than what we are use to here. For example ... The Albaicin neighborhood is where we plan to live like we’ve mentioned before. So why the Albaicin? The Albaicin is a Medieval Moorish area that dates back to the Nasrid Kingdom. It has narrow winding streets on a hill with little access to cars, and it was declared a World Heritage Site by UNESCO in 1994. We love the history and that it is so different than what the kids / we are use to now.

-Size (Population 240,000+)

-University City (University of Granada) ... A university brings in an international population and even more cultural / educational opportunities.

-History / Cultural / The Arts (The Alhambra being the most exciting destination. A castle in our backyard? Can’t beat that!).

-One of the last remaining cities in Spain with complementary tapas!

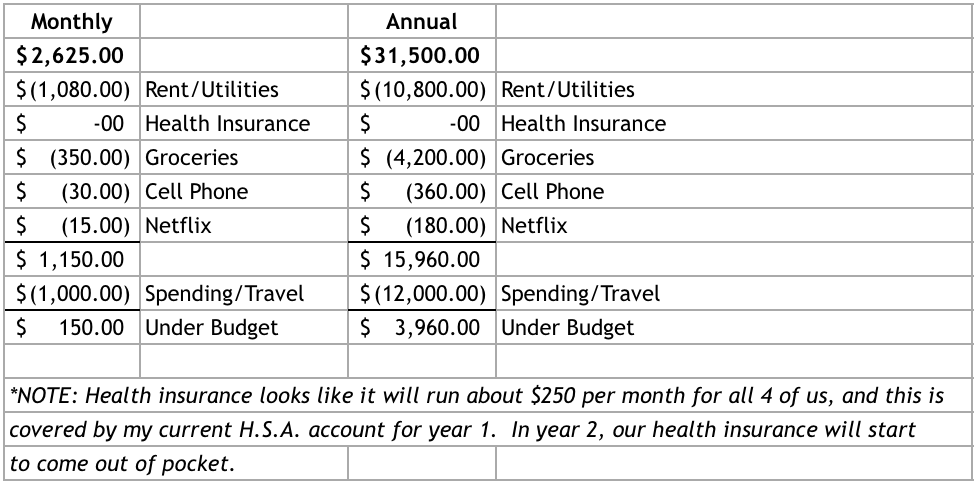

-Cost of living.

-Our kids are currently involved in golf and dance ... and both are available in Granada (and of course we would like them try new activities too. Spanish guitar? Flamenco?). For example, Granada Club de Golf is close by. And this school ... Lucia Guarnido may be a good dance school for our youngest offering both ballet and flamenco (and more). I need to research both more, but I like what I see.

-Other American families have gone for sabbaticals (with kids) such as the family from Bucking the Trend. We’ve also talked to families that have stayed more recently, and some that are there right now!

-And with the help of some expats currently there, I’ve researched and found what I think will be a great school for the kids (more on that one another time!).

Other perks?

-It is only about a 2 hour (or less) bus ride to Malaga (Picasso’s hometown!).

-So close and easy to access Morocco! We can’t stay in Granada without a visit to Morocco.

And what about negatives? The biggest negative has nothing to do with Spain or Granada (temporary distance between loved ones... come visit!), but every place has drawbacks, right? The biggest “cons” I’ve heard / read about from American expats are ... slow process / red tape when dealing with city / government so we will just have to practice our patience. And the other one we hear which is really more of a plus to me (and many expats) ... you have to get use to a slower way of life versus the typical American lifestyle. Stop and smell the roses versus go, go, go... I see that as a plus! But I’ve heard it takes some getting use to being able to slow yourself down.

So there you have it. What was top of mind for us? ... Top of mind for us is climate / seasons, and we wanted to be able to enjoy the outdoors (it does get hot in Granada, but we plan to be back in the US visiting family during those months ... July and August). We also wanted to be in a city that wasn’t too large right now (so therefore, not Madrid) with the ability to walk and access to public transportation. (I love big cities (Houston is the 4th largest in the US!), but our goal right now is to do something different. Besides the weather in Houston (too hot May - September), my other biggest complaint is how spread out it is (always driving) ...and lack of public transportation (and lack of the ability to walk). I love being able to step out my door (hello, NYC!) and let my feet take me where I need to go. I am an art teacher and love the arts ....so access to great arts / culture / education is a top priority for me too. And of course there is a financial aspect to our decision ... the cost of living in Granada is very affordable if not better than what we are use to in Houston.

If you (when you!) reach financial independence and had the ability and time to go anywhere, where would you go? Why? What would be top of mind for you?

And how to reach financial independence again?

Step 1: Eliminate debt.

Step 2: Figure out your magic FI number! What amount do you need to achieve financial independence?

Step 3: Reduce spending and achieve high savings rate.

Step 4: Invest, invest, invest (once you eliminate debt).

Step 5: Reach your FI number and enjoy FIRE! (Need help getting there? Read more about how we can help.)

-Tara